hanimmal

Well-Known Member

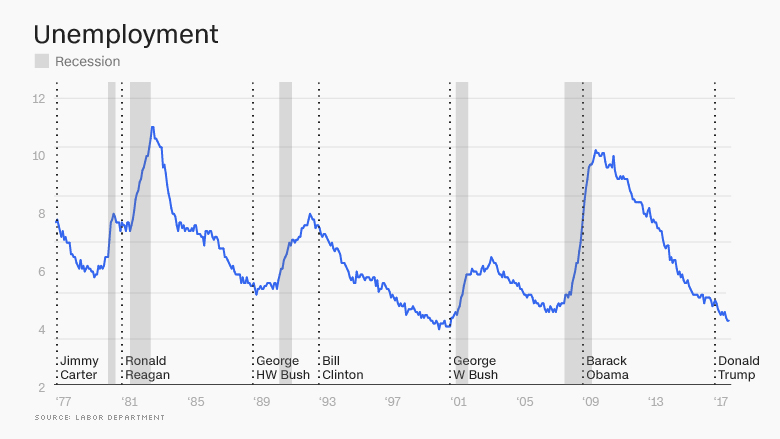

The Republicans seem to love dumping a recession on the American economy.

https://www.washingtonpost.com/opinions/2020/04/02/another-gop-president-another-recession/

https://www.washingtonpost.com/opinions/2020/04/02/another-gop-president-another-recession/

President Trump did not create the coronavirus, but his failure to act swiftly and implement extensive testing and contact tracing left us with one option: extreme social distancing. And naturally, social distancing meant the economy ground to a halt. In that sense, the recession is a product of Trump’s mismanagement and willful ignorance. And that recession will be frightfully severe.

Full coverage of the coronavirus pandemic

The Post reports: “More than 6.6 million Americans applied for unemployment benefits last week — a record — as political and public health leaders put the economy in a deep freeze, keeping people at home and trying to slow the spread of the deadly coronavirus.” The magnitude of the job losses so far — and there will be more to come — is staggering. (“The past two weeks have erased nearly all the jobs created in the past five years, a sign of how rapid, deep and painful the economic shutdown has been on many American families who are struggling to pay rent and health insurance costs in the midst of a pandemic.”) The number of claims so far, more than 10 million, is likely understated “since a lot of newly unemployed Americans haven’t been able to fill out a claim yet.”

As businesses find they can no longer hold out, declare bankruptcy or shut their doors, more people will lose their jobs. Employees asked to take pay cuts one month will find that their employer in a month or two can no longer keep them on payroll at all.

In looking at the political implications of this horror show, one need only recall the 2008 Great Recession. The causes of that financial collapse — e.g., unregulated financial instruments, negligence from ratings companies, lender deception, the Federal Reserve’s failure to act — were complicated. Nevertheless, the politicians who resisted warnings (from then-Harvard professor Elizabeth Warren, among other people) and favored a Wild West deregulated financial industry have unique culpability. And the party in charge at the time — the Republicans — bore the brunt of the voters wrath at the polls. Do we imagine this domestic debacle will play out differently?

Trump and his Republicans are vulnerable on three counts: failure to act to head off the pandemic, failure to respond adequately to the crisis and corruption in the response (in an administration already infamous for corruption and self-dealing).

Senate Majority Leader Mitch McConnell (R-Ky.), among Trump’s most fervent enablers, picked a poor time to declare that the federal government should stop helping. The Post’s Robert Costa reports that McConnell delivered a “sweeping dismissal” of the call from House Speaker Nancy Pelosi (D-Calif.) for a fourth stimulus package:

At her weekly news conference, she was even more emphatic, both on continuing to fund the recovery and on clamping down on corruption. She urged more money for equipment for health-care responders and other “front-line workers,” funds for states to manage unemployment insurance claims and a major effort on infrastructure (including water, broadband and community health-care centers). Reacting to the unemployment claims, she asked, “Does that just not take your breath away?” As for McConnell, she said bluntly, “We’ll have our bill.”

The Opinions section is looking for stories of how the coronavirus has affected people of all walks of life. Write to us.

Perhaps most important, Pelosi will set up a House select committee to oversee the entire coronavirus effort, much like then-Sen. Harry Truman did for World War II funding, to crack down on waste, fraud and abuse.

https://www.washingtonpost.com/opinions/2020/04/02/another-gop-president-another-recession/President Trump did not create the coronavirus, but his failure to act swiftly and implement extensive testing and contact tracing left us with one option: extreme social distancing. And naturally, social distancing meant the economy ground to a halt. In that sense, the recession is a product of Trump’s mismanagement and willful ignorance. And that recession will be frightfully severe.

Full coverage of the coronavirus pandemic

The Post reports: “More than 6.6 million Americans applied for unemployment benefits last week — a record — as political and public health leaders put the economy in a deep freeze, keeping people at home and trying to slow the spread of the deadly coronavirus.” The magnitude of the job losses so far — and there will be more to come — is staggering. (“The past two weeks have erased nearly all the jobs created in the past five years, a sign of how rapid, deep and painful the economic shutdown has been on many American families who are struggling to pay rent and health insurance costs in the midst of a pandemic.”) The number of claims so far, more than 10 million, is likely understated “since a lot of newly unemployed Americans haven’t been able to fill out a claim yet.”

As businesses find they can no longer hold out, declare bankruptcy or shut their doors, more people will lose their jobs. Employees asked to take pay cuts one month will find that their employer in a month or two can no longer keep them on payroll at all.

In looking at the political implications of this horror show, one need only recall the 2008 Great Recession. The causes of that financial collapse — e.g., unregulated financial instruments, negligence from ratings companies, lender deception, the Federal Reserve’s failure to act — were complicated. Nevertheless, the politicians who resisted warnings (from then-Harvard professor Elizabeth Warren, among other people) and favored a Wild West deregulated financial industry have unique culpability. And the party in charge at the time — the Republicans — bore the brunt of the voters wrath at the polls. Do we imagine this domestic debacle will play out differently?

Trump and his Republicans are vulnerable on three counts: failure to act to head off the pandemic, failure to respond adequately to the crisis and corruption in the response (in an administration already infamous for corruption and self-dealing).

Senate Majority Leader Mitch McConnell (R-Ky.), among Trump’s most fervent enablers, picked a poor time to declare that the federal government should stop helping. The Post’s Robert Costa reports that McConnell delivered a “sweeping dismissal” of the call from House Speaker Nancy Pelosi (D-Calif.) for a fourth stimulus package:

In her initial written response, Pelosi said, “The victims of the coronavirus pandemic cannot wait. It is moving faster than the leader may have suspected, and even he has said that some things should wait for the next bill.”“She needs to stand down on the notion that we’re going to go along with taking advantage of the crisis to do things that are unrelated to the crisis,” McConnell said in an interview with The Washington Post, calling the speaker’s recent comments about a fourth round of virus-related legislation “premature.”

At her weekly news conference, she was even more emphatic, both on continuing to fund the recovery and on clamping down on corruption. She urged more money for equipment for health-care responders and other “front-line workers,” funds for states to manage unemployment insurance claims and a major effort on infrastructure (including water, broadband and community health-care centers). Reacting to the unemployment claims, she asked, “Does that just not take your breath away?” As for McConnell, she said bluntly, “We’ll have our bill.”

The Opinions section is looking for stories of how the coronavirus has affected people of all walks of life. Write to us.

Perhaps most important, Pelosi will set up a House select committee to oversee the entire coronavirus effort, much like then-Sen. Harry Truman did for World War II funding, to crack down on waste, fraud and abuse.